Exxon Mobil Corporation (NYSE: XOM) and Pioneer Natural Resources (NYSE: PXD) jointly announced a definitive agreement for ExxonMobil to acquire Pioneer. The merger is an all-stock transaction valued at $59.5 billion, or $253 per share, based on ExxonMobil’s closing price on October 5, 2023. Under the terms of the agreement, Pioneer shareholders will receive 2.3234 shares of ExxonMobil for each Pioneer share at closing. The implied total enterprise value of the transaction, including net debt, is approximately $64.5 billion

Data Download Center

Oil & Gas Operators in the US

List ofd active Oil & Gas Operators active in the US

- Transforms ExxonMobil’s upstream portfolio, more than doubling the company’s Permian footprint and creating an industry-leading, high-quality, high-return undeveloped U.S. unconventional inventory position

- Expect to generate double-digit returns by recovering more resource, more efficiently and with a lower environmental impact

- Combines Pioneer’s sizeable acreage, entrepreneurial culture and deep industry expertise with ExxonMobil’s balance-sheet strength, advanced technologies and industry-leading project development capabilities

- Plans to accelerate Pioneer’s net zero Permian ambition from 2050 to 2035

- Strengthens U.S. economy and energy security

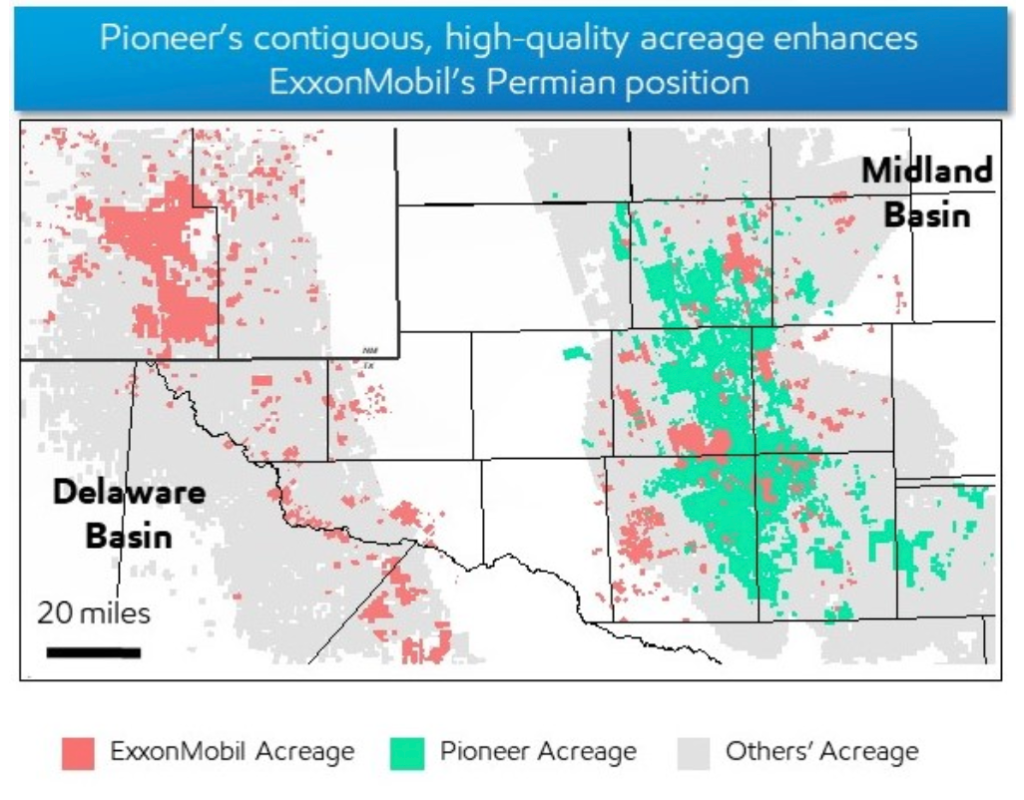

The merger combines Pioneer’s more than 850,000 net acres in the Midland Basin with ExxonMobil’s 570,000 net acres in the Delaware and Midland Basins, creating the industry’s leading high-quality undeveloped U.S. unconventional inventory position. Together, the companies will have an estimated 16 billion barrels of oil equivalent resource in the Permian. At close, ExxonMobil’s Permian production volume would more than double to 1.3 million barrels of oil equivalent per day (MOEBD), based on 2023 volumes, and is expected to increase to approximately 2 MOEBD in 2027. ExxonMobil believes the transaction represents an opportunity for even greater U.S. energy security by bringing the best technologies, operational excellence and financial capability to an important source of domestic supply, benefitting the American economy and its consumers.

The merger combines Pioneer’s more than 850,000 net acres in the Midland Basin with ExxonMobil’s 570,000 net acres in the Delaware and Midland Basins, creating the industry’s leading high-quality undeveloped U.S. unconventional inventory position. Together, the companies will have an estimated 16 billion barrels of oil equivalent resource in the Permian. At close, ExxonMobil’s Permian production volume would more than double to 1.3 million barrels of oil equivalent per day (MOEBD), based on 2023 volumes, and is expected to increase to approximately 2 MOEBD in 2027. ExxonMobil believes the transaction represents an opportunity for even greater U.S. energy security by bringing the best technologies, operational excellence and financial capability to an important source of domestic supply, benefitting the American economy and its consumers.

Pioneer Chief Executive Officer Scott Sheffield commented, “The combination of ExxonMobil and Pioneer creates a diversified energy company with the largest footprint of high-return wells in the Permian Basin. As part of a global enterprise, Pioneer, our shareholders and our employees will be better positioned for long-term success through a size and scale that spans the globe and offers diversity through product and exposure to the full energy value chain. The consolidated company will maintain its leadership position, driving further efficiencies through the combination of our adjacent, contiguous acreage in the Midland Basin and our highly talented employee base, with the improved ability to deliver durable returns, creating tangible value for shareholders for decades to come.”

Combining Pioneer’s differentiated Permian inventory and basin knowledge with ExxonMobil’s proprietary technologies, financial resources, and industry-leading project development is expected to generate double-digit returns by recovering more resource, more efficiently and with a lower environmental impact.

The transaction is a unique opportunity to deliver leading capital efficiency and cost performance as well as increase production by combining Pioneer’s large-scale, contiguous, high-quality undeveloped Midland acreage with ExxonMobil’s demonstrated industry-leading Permian resource development approach.

The unique, complementary fit of Pioneer’s contiguous acreage will allow ExxonMobil to drill long, best-in-class laterals — up to four miles — which will result in fewer wells and a smaller surface footprint. The company also expects to enhance field digitalization and automation that will optimize production throughput and cost.

The combination transforms ExxonMobil’s upstream portfolio by increasing lower-cost-of-supply production, as well as short-cycle capital flexibility. The company expects a cost of supply of less than $35 per barrel from Pioneer’s assets. By 2027, short-cycle barrels will comprise more than 40% of the total upstream volumes, positioning the company to more quickly respond to demand changes and increase capture of price and volume upside.

The transaction’s unique value creation opportunity results in significant synergies and further upside potential that will be shared by both companies’ shareholders. The merger is anticipated to be accretive immediately and highly accretive mid- to long-term to ExxonMobil earnings per share and free cash flow, with a long cash flow runway. ExxonMobil’s strong balance sheet combined with Pioneer’s added surplus free cash flow provides upside opportunity to enhance shareholder capital returns post-closing.

Finally, this merger represents the opportunity for even greater U.S. energy security by bringing the best technology, operational excellence, environmental best practices and financial capability to an important source of domestic supply, benefitting the American economy and its consumers.

Accelerating to Net Zero in the Permian

ExxonMobil has industry-leading plans to achieve net zero Scope 1 and Scope 2 greenhouse gas emissions from its Permian unconventional operations by 2030. As part of the transaction, ExxonMobil intends to leverage its Permian greenhouse gas reduction plans to accelerate Pioneer’s net zero emissions plan by 15 years, to 2035.

ExxonMobil will leverage the same aggressive strategy and apply its industry-leading new technologies for monitoring, measuring, and addressing fugitive methane to lower both companies’ methane emissions.

In addition, using combined operating capabilities and infrastructure, we expect to increase the amount of recycled water used in our Permian fracturing operations to more than 90% by 2030.

Transaction Details

The per-share merger consideration noted above represents an approximate 18% premium to Pioneer’s undisturbed closing price on October 5 and a 9% premium to its prior 30-day volume-weighted average price on the same day.

The Boards of Directors of both companies have unanimously approved the transaction, which is subject to customary regulatory reviews and approvals. It is also subject to approval by Pioneer shareholders. The transaction is expected to close in the first half of 2024.

Energy News

Author: phinds