Crescent Point Announces Accretive Acquisition of Shell Kaybob Duvernay Assets

Download Well & Facility Permits

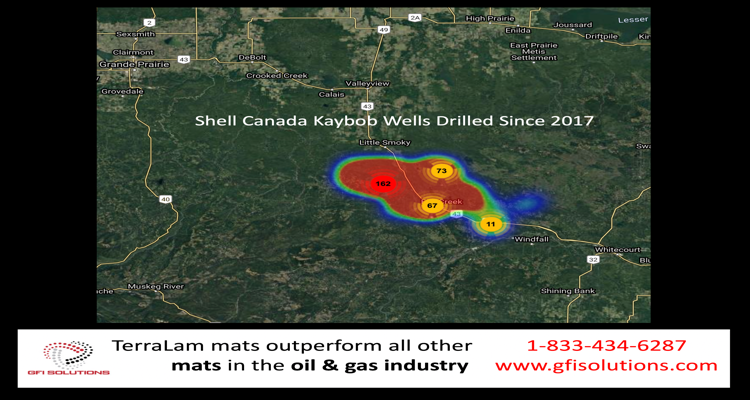

Get the well permits, wells drilled and facility permits for Shell Kaybob last 3 years

CALGARY, AB, Feb. 17, 2021 /CNW/ – Crescent Point Energy Corp. (“Crescent Point” or the “Company”) (TSX: CPG) (NYSE: CPG) is pleased to announce that it has entered into an agreement (the “Agreement”) with Shell Canada Energy (“Shell”), an affiliate of Royal Dutch Shell plc, to acquire Shell’s Kaybob Duvernay assets in Alberta (the “Assets”) for $900 million (the “Acquisition”). The total consideration consists of $700 million in cash and 50 million common shares of Crescent Point.

KEY HIGHLIGHTS

- Strategic entry into a premier and established liquids rich play with greater than 10 years of high-return, low risk drilling inventory.

- Strengthens expected 2021 excess cash flow generation to approximately $375 to $600 million, at US$50/bbl to US$60/bbl WTI.

- Pro-forma 2021 guidance production of approximately 134,000 boe/d, primarily comprised of high-margin oil and liquids.

- Improves netback by over seven percent by lowering royalty rates and reducing per boe operating and G&A expenses.

- Lowers expected year-end 2021 leverage to approximately 2.3 to 1.6 times adjusted funds flow, at US$50/bbl to US$60/bbl WTI.

- Enhances ESG profile through Assets with a low standing well count with minimal reclamation and a low emissions intensity.

Sponsor

GFI Solutions provides TerraLam Cross Laminated Timber (CLT) Access mats for rental or purchase. We have service locations and highly skilled personnel strategically located across Western Canada to ensure your specifications are met.

NO DAMAGE & NO REPLACEMENT COST GUARANTEE Our matting is so strong we won’t charge for ANY damage or replacement costs. With the most efficient crews in the industry backed by 24/7 service and support your mats will be installed faster with safety in mind.

STRATEGIC RATIONALE AND ASSET OVERVIEW

“We are excited to add the Kaybob Duvernay asset as a strategic core area to our portfolio, as its significant inventory of high-return locations and free cash flow profile provide an attractive and return enhancing opportunity for our shareholders,” said Craig Bryksa, President and CEO of Crescent Point. “The Acquisition is aligned with our core principles to focus on strategic initiatives that enhance our balance sheet strength and sustainability. It is expected to enhance our free cash flow generation, leverage ratios and ESG profile. The depth of high-return drilling inventory also provides optionality within our capital allocation framework. We view the Kaybob assets as low-risk given that they have been delineated over the past decade and key infrastructure and market access are already in place.”

Key attributes of the acquired Assets include the following:

- Production of approximately 30,000 boe/d (57% condensate, 8% NGL and 35% shale gas);

- Core of the condensate rich fairway with attractive reservoir characteristics, including higher pressure and pay thickness;

- Approximately 500 net sections of contiguous land in the Kaybob area (approximately 325 net sections undeveloped);

- 98 percent Crown land with limited expiry concerns and a high working interest of approximately 100 percent;

- Approximately 200 net internally identified drilling locations, based on conservative well spacing of 600 meters, of which only 36 are booked as Proved plus Probable (“2P”) in the independent evaluators report prepared by McDaniel & Associates Consultants Ltd. (the “McDaniel Report”). These locations are primarily comprised of two-mile horizontal wells;

- High quality type wells with strong liquids rates and competitive full-cycle economics;

- Significant owned and third party infrastructure currently in place, leading to lower expected future capital requirements; and

- A royalty rate of approximately five percent and expected operating expenses of approximately $7.25 per boe.

Prior to the expected closing of the Acquisition in April 2021, Shell plans to bring a number of drilled and uncompleted wells on stream. As a result, production from the acquired Assets is expected to increase to approximately 35,000 boe/d during second quarter 2021. Crescent Point plans to manage these Assets to target a lower decline rate and longer-term production of approximately 30,000 boe/d. Following the initial period of flush production, the Company’s pro-forma decline rate is expected to remain unchanged at approximately 25 percent.

Crescent Point will also seek opportunities to enhance returns over time through potential operational efficiencies and effective knowledge transfer. Crescent Point will combine its significant expertise in multi-well pad development and field technology, including experience gained from other North American resource plays with similar geology, along with the technical expertise provided by the Shell staff that will be joining the Company.

TRANSACTION DETAILS, METRICS AND FINANCIAL ACCRETION

As part of this Agreement, Crescent Point has agreed to acquire the Assets for $900 million. The Acquisition will be funded through a combination of $700 million in cash, accessed through the Company’s credit facility, and 50 million Crescent Point common shares. Upon closing, Shell will own approximately 8.6 percent of the outstanding Crescent Point common shares.

With approximately 30,000 boe/d of production and assuming US$50/bbl WTI, the estimated acquisition metrics are as follows:

- Less than 3.0 times net operating income based on an operating netback of approximately $30 per boe;

- $30,000 per flowing boe; and

- $12.87 per boe of 2P reserves of 107.4 MMboe as assigned by the independent evaluator, equating to a recycle ratio of over 2.0 times, including $483 million of undiscounted future development capital.

The acquired Assets are estimated to require approximately $180 million of annual capital to sustain approximately 30,000 boe/d of production, further enhancing the Company’s free cash flow generation.

This Acquisition is expected to be accretive on all per share metrics. In particular, in the 12 month period following the closing of the Acquisition, excess cash flow per share is expected to double with adjusted funds flow per share increasing by greater than 25 percent, compared to Crescent Point’s pre-acquisition expectations. These accretion metrics improve further on a debt-adjusted basis. In addition, the Company’s adjusted funds flow netback is also expected to increase by over seven percent, driven by a lower royalty rate and anticipated per boe operating and general and administrative expense reductions.

The above mentioned transaction metrics and financial accretion are based on a price forecast of US$50/bbl WTI, CDN$2.50/mcf AECO and a US$/CDN $0.78 exchange rate. The effective date of the Acquisition is January 1, 2021.

Scotiabank and BMO Capital Markets acted as financial advisors to Crescent Point on this transaction. The Acquisition is subject to the satisfaction of customary closing conditions, consents and regulatory approvals.

BALANCE SHEET AND FINANCIAL FLEXIBILITY

Crescent Point’s pro-forma leverage ratio is expected to improve to approximately 2.3 to 1.6 times net debt to adjusted funds flow at the end of 2021, based on US$50/bbl to US$60/bbl WTI.

Upon closing of the Acquisition, Crescent Point’s unutilized credit capacity on its current facilities is expected to total approximately $2.0 billion. The Company will continue to prioritize its balance sheet with the allocation of its excess cash flow and will remain active on potential acquisitions and dispositions as part of its focused asset strategy.

COMMITMENT TO ENVIRONMENTAL, SOCIAL AND GOVERNANCE (“ESG”)

Crescent Point’s purpose for ‘Bringing energy to our world – the right way’ highlights the Company’s role to produce responsibly developed energy with ESG standards being top of mind.

This Acquisition further bolsters Crescent Point’s ESG profile due to the low standing well count and minimal undiscounted uninflated asset retirement obligations of approximately $50 million associated with the Assets. The Liability Management Rating (“LMR”) associated with these Assets is 7.9, well above the peer average in Alberta. The Company’s corporate emissions intensity is also expected to improve with the addition of the Assets.

UPDATED 2021 GUIDANCE AND EXCESS CASH FLOW GENERATION

Crescent Point’s revised annual guidance for 2021, which incorporates the impact of the announced Acquisition for the remainder of the year, assuming the anticipated closing in April 2021, includes annual average production of 132,000 to 136,000 boe/d and development capital expenditures of $575 million to $625 million. The Company’s revised budget includes approximately $100 million of development capital expenditures expected to be directed to the newly acquired Kaybob Duvernay assets, with the balance of its program remaining unchanged from prior guidance.

On an annual pro-forma basis, Crescent Point’s sustaining development capital expenditures are now expected to be approximately $800 to $850 million to generate annual production that is in-line with, or exceeds, the current 2021 annual guidance range.

The Company’s revised 2021 guidance is now expected to generate excess cash flow of approximately $375 million to $600 million, at US$50/bbl to US$60/bbl WTI, providing an increased opportunity to further enhance shareholder value. The Company will have approximately 30 percent of its pro-forma oil and liquids production, net of royalty interest, hedged through the remainder of 2021 upon closing of the Acquisition.

Author: phinds

Pingback:Mid-con Wells Spud - download full report – Oil Gas Leads

Pingback:Spartan Delta buys Inception Exploration and oil and gas assets for $148 million - download well & facility permits – Oil Gas Leads

Pingback:Western Canada Well Permits – Oil Gas Leads

Pingback:Western Canada Rig Report - download report – Oil Gas Leads

Pingback:Whitecap Resources FULL YEAR 2021 GUIDANCE - download well permits & facility permits – Oil Gas Leads

Pingback:Crescent Point Energy Corp. Q1 2021 update – English Times