In a story that should surprise no one, the Wall Street Journal and others are reporting that the long-anticipated deal between U.S. energy giant ExxonMobilXOM -1.7% and Permian Basin titan Pioneer Natural ResourcesPXD +10.5% could finally be upon us.

Data Download Center

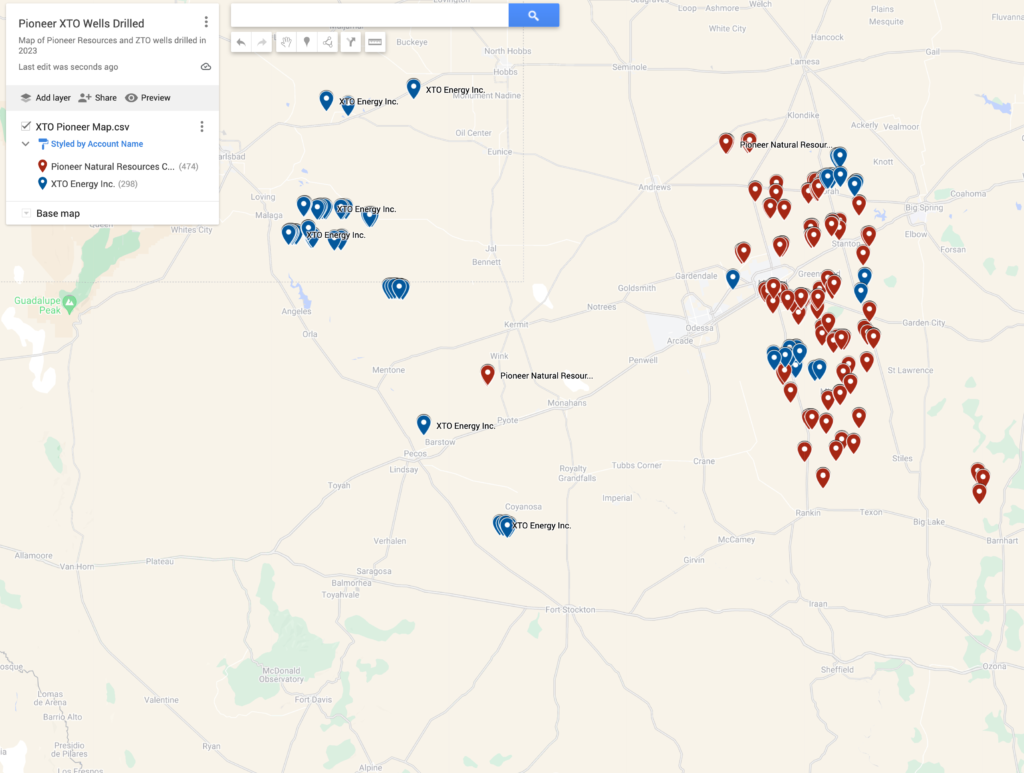

XTO/Pioneer wells drilled in 2023

Detailed list of wells drilled by Pioneer and XTO in 2023

Permian Basin Oil & Gas Operators

Detailed list of Operators active in the Permian Basin

Rumors about a possible deal between the two companies have circulated off and on since at least 2017, and heated up again this past April. But, as with so many times before, the rumors soon cooled down when no deal was consummated. Perhaps this time will be different, but only time will tell.

Pioneer XTO Wells Drilled 2023 Map (click to access)

As of close of business Thursday, Pioneer boasted a market cap of more than $50 billion, meaning it would become Exxon’s biggest acquisition since its $81 billion merger with Mobil Oil Company in 1998. If completed, this deal would easily surpass ExxonMobil’s $41 billion buyout of Fort Worth-based independent XTO Energy in 2009.

A merger between the two companies would also cement the combined company as far and away the dominant producer in the Permian Basin, the world’s most active oil and gas play. Pioneer has long ranked as the biggest holder of leases and drilling opportunities in the Midland sub-basin of the greater Permian Basin region, while ExxonMobil owns substantial leasehold in both the Midland and Delaware basins.

An ExxonMobil/Pioneer deal would signify the continuation of the ‘bigger is better’ philosophy that has dominated the shale oil and gas sector in recent years. That has been the dominant theme as upstream companies have sought to grow through acquisitions as the main means of maintaining their inventories of future drilling projects. Growth via M&A also provides opportunities to optimize head counts and take advantage of other economies of scale and operational efficiencies.

The large amount of contiguous acreage owned by the two companies would allow ExxonMobil to optimize water usage, recycling and transport operations, minimize the number of truck trips related to each specific task, and maximize efficiencies related to both drilling and hydraulic fracturing scheduling, among an array of additional efficiencies.

For its own part, Pioneer has also been active in the growth via acquisitions space, executing buyouts of both Parsley Energy and DoublePoint Energy for a combined $11 billion during 2021. The company has grown to become the largest pure-play Permian Basin company under the leadership of longtime CEO Scott Sheffield.

A deal with Pioneer would come just three months after ExxonMobil’s last big acquisition, the $4.9 billion buyout of midstream company Denbury in July. That deal was another natural fit for the energy giant, mainly additive to its Low Carbon Ventures (LCV) business unit, given Denbury’s suite of CO2 pipelines and other CO2-related assets. Exxon’s LCV unit has a heavy focus on mounting major carbon capture and storage projects along the Texas and Louisiana Gulf Coast, where much of the Denbury assets are located.

But a deal with Pioneer would be all about oil and gas, all about the upstream, and all about the prolific Permian Basin. It would also be entirely consistent with the beefed-up, Permian-heavy capital budget Exxon and its CEO, Darren Woods, rolled out early this year.

This is a deal that has always seemed like a natural fit but has never managed to come to fruition. Perhaps this time will be the charm.

[Update] Andrew Dittmar, Manager at energy and analytics firm at Enverus, has this to say about the rumored merger in an email:

“We view the potential merger, which would carry a price tag of $60 billion according to the Wall Street Journal, as a significant win for XOM and a reasonable conclusion for PXD at a reported ~9% premium to its share price at its prior-day close. We have long viewed XOM as the most likely first-mover buyer in large-scale Permian M&A, due in part to its aggressive growth targets, in addition to viewing PXD as its ideal acquisition candidate.”

He estimates that PXD owns “6,300 net locations of high-quality inventory (well locations that generate a 10% return at a WTI price of below $50), or 16 years of drilling activity at its current rig cadence. Such duration of operated inventory leads oil-weighted shale producers and would be significantly accretive to XOM’s duration.”

Dittmar notes that the rumored price for Pioneer implies that ExxonMobil is paying a significant premium per location over other recent Permian-centric M&A deals. But he points out that those prior deals were not really comparable in terms of scale or inventory duration.

Dittmar also thinks this deal, if completed, c0uld spur other big Permian players to pursue deals of their own. “The key implication for the rest of the sector, in our view, would be setting a precedent for a reasonable premium in large-scale M&A. We suspect other large-caps that are hungry for inventory would view the deal positively for any efforts to pursue similar deals.”

Energy News

Author: phinds