Pioneer Natural Resources Company announced acquisition of DoublePoint Energy (DoublePoint) in the Midland Basin a transaction valued at approximately $6.4 billion.

The deal is comprised of approximately 27.2 million shares of Pioneer common stock, $1 billion of cash and the assumption of approximately $0.9 billion of debt and liabilities.

Scott D. Sheffield, Pioneer’s CEO stated, “DoublePoint has amassed an impressive, high quality footprint in the Midland Basin, comprised of tier one acreage adjacent to Pioneer’s leading position. We are pleased with their decision to become long-term partners with Pioneer in a transaction that will complement our unmatched position in the core of the Permian Basin. Pioneer will incorporate these assets into our investment model, migrating the assets from significant production growth to a free cash flow model, moderating growth for the U.S. shale industry and generating significant value for our shareholders.”

Pioneer Natural Resources Company and DoublePoint Energy Well Permits Download

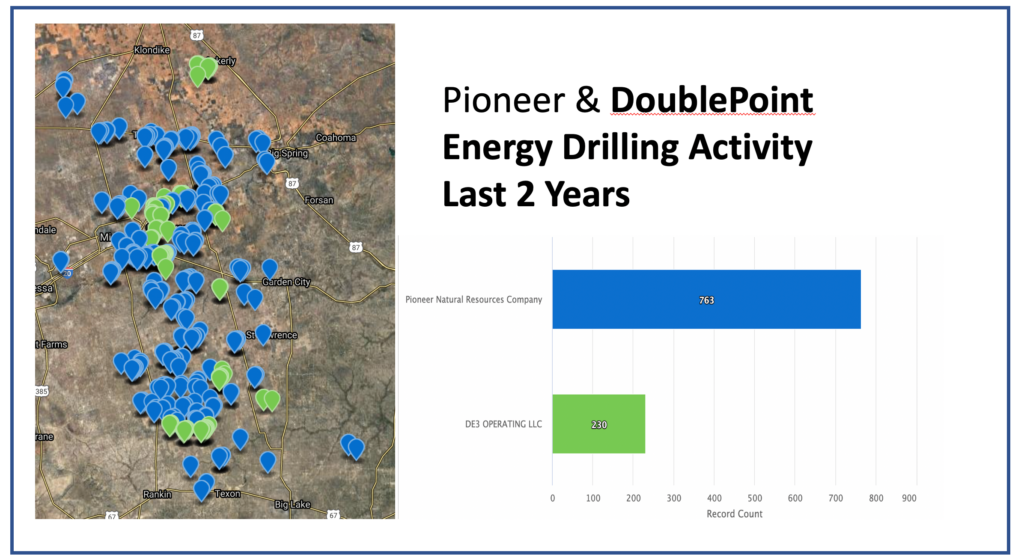

Pioneer Natural Resources Company and DoublePoint Energy Map of Wells Drilled Last 2 Years

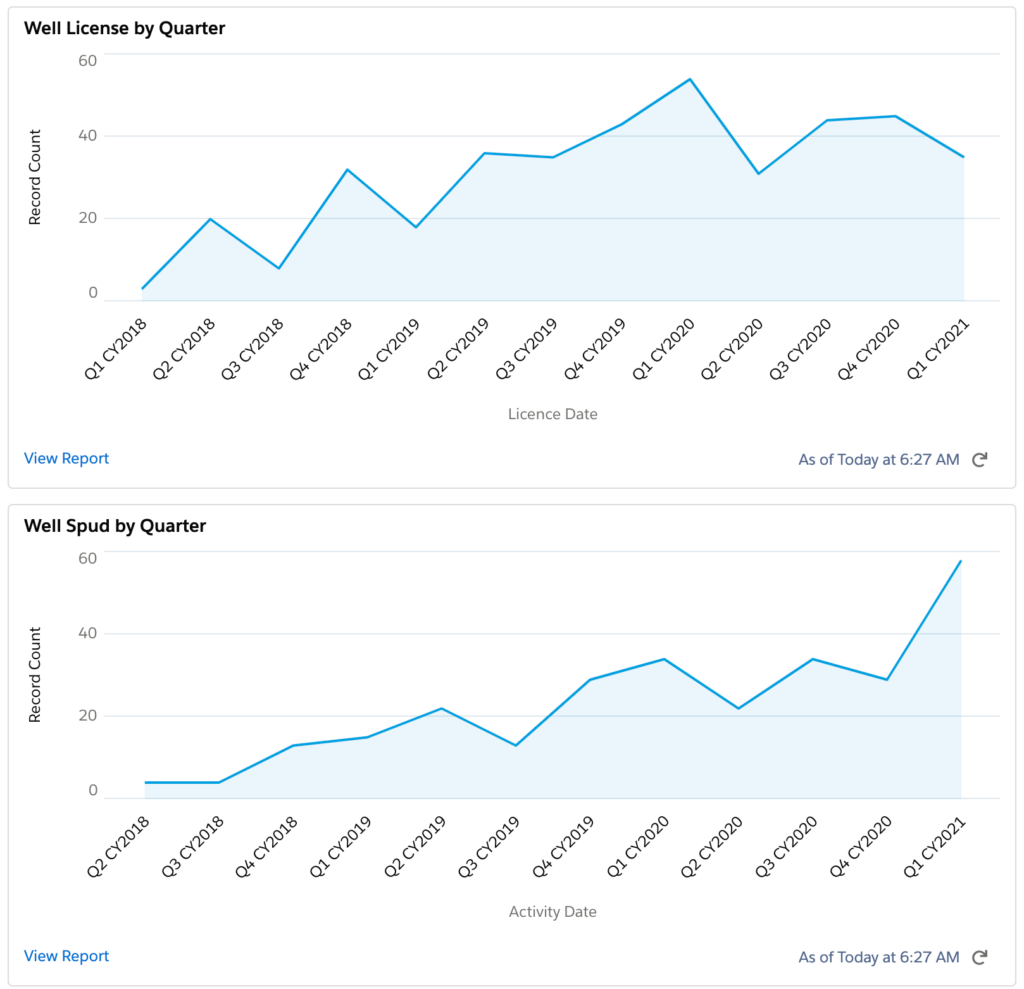

DoublePoint Energy Well Permits and Wells Drilled Chart

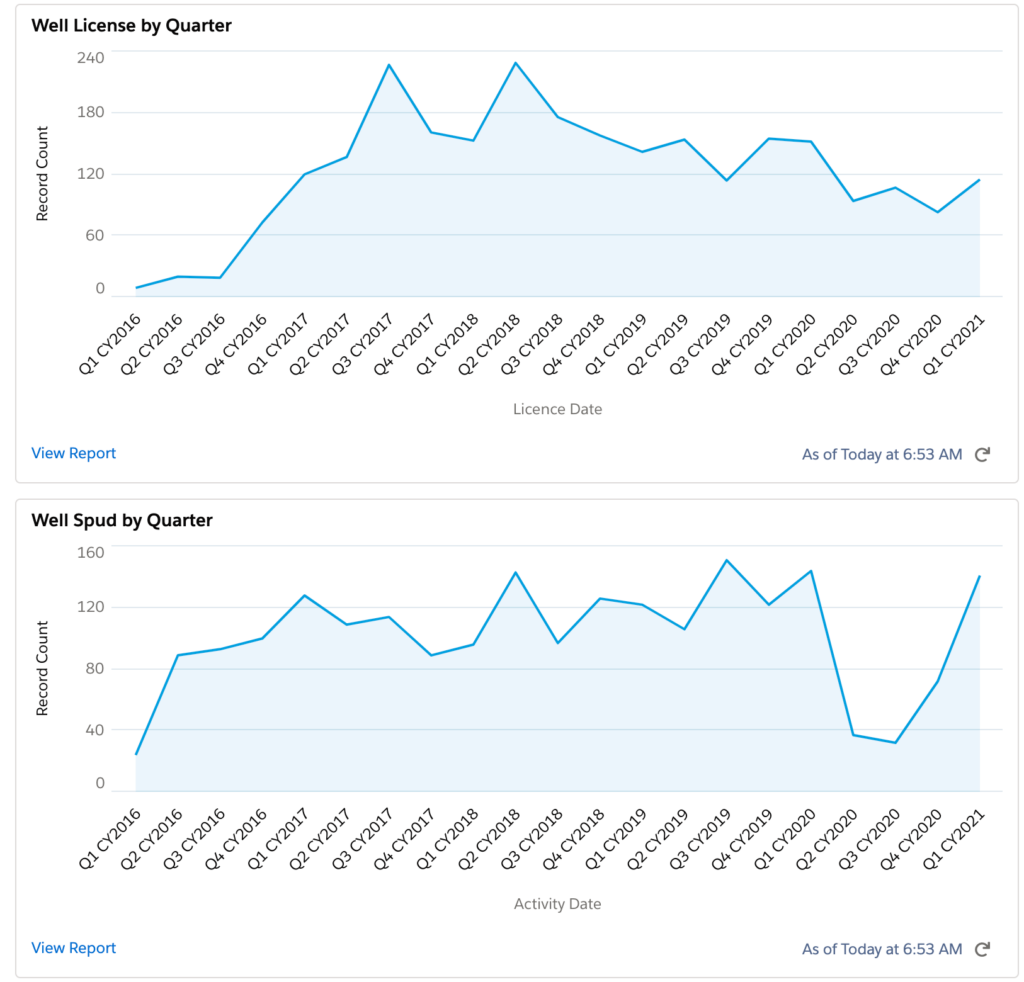

Pioneer Natural Resources Well Permits and Wells Drilled Chart

Transaction Enhances Investment Framework

- Accretive to Key Financial Metrics – Pioneer expects the transaction to be accretive on key financial metrics including cash flow and free cash flow per share, earnings per share and corporate returns during 2021 and beyond.

- Increases Variable Dividend Outlook – Consistent with Pioneer’s priority of returning capital to shareholders, the accretive nature of this transaction to free cash flow leads to an increase in the expected per share variable dividend beginning in 2022 and beyond.

- Unmatched Permian Scale – This transaction represents a contiguous position of approximately 97,000 high quality net acres directly offsetting and overlapping Pioneer’s existing footprint. The acquired acreage is primarily undrilled and augments Pioneer’s premium asset base, increasing the Company’s acreage position to greater than 1 million net acres with no exposure to federal lands. The Company expects production from the acquired assets to reach approximately 100,000 barrels of oil equivalent per day by late in the second quarter.

- Significant Synergies – The acquisition is expected to result in annual cost savings of approximately $175 million through operational efficiencies and reductions in general and administrative (G&A) and interest expenses. The expected present value of these cost savings totals approximately $1 billion over a 10-year period.

- Top-Tier Balance Sheet Maintained – Pioneer’s pro forma leverage metrics will remain relatively unchanged, among the lowest in the industry, preserving the Company’s financial and operational flexibility and allowing for significant return of capital to shareholders.

Geoffrey Strong, Senior Partner and Co-Head of Infrastructure and Natural Resources at Apollo, commented, “The combination of Pioneer and DoublePoint is compelling from both a financial and operational standpoint and a natural fit for DoublePoint. This acquisition continues the trend of consolidation in the prolific Permian Basin, combining two complementary footprints in a transaction with both top- and bottom-line synergies.” Dheeraj Verma, President of Quantum Energy Partners added, “we are firm believers in Pioneer’s strategy of free cash flow generation, which enables a competitive base and strong variable dividend.”

Cody Campbell and John Sellers, Co-CEO’s of DoublePoint Energy said, “We are proud and appreciative of the work that our team has done to build a company and an asset base that is unparalleled in quality and truly cannot be replicated. We are honored to have the opportunity to combine our business with Pioneer, who we have long admired and regard as the premiere operator in the Midland Basin. The fit and the synergies are clear, and we look forward to working with Pioneer to continue creating value.”

Transaction Details

Pioneer will issue approximately 27.2 million shares of common stock in the transaction with an additional $1 billion of cash. After closing, existing Pioneer shareholders will own approximately 89% of the combined company and existing DoublePoint owners will own approximately 11% of the combined company. Pioneer plans to finance the cash portion of the purchase price through a combination of cash on-hand and existing borrowing capacity under its revolving credit facility.

The transaction has been unanimously approved Pioneer’s Board of Directors and is expected to close in the second quarter of 2021, subject to customary closing conditions and regulatory approvals.

The transaction is structured as the acquisition by a Pioneer subsidiary of 100% of the limited liability company interests of DoublePoint’s wholly owned subsidiary, Double Eagle III Midco 1 LLC.

Oil & Gas News

Sign-up Free Weekly Oil & Gas Permit eMail

* These fields are required.

Author: phinds