HIGHLIGHTS

Will ‘ramp up a little bit’ in both plays: CEO

Price per acre favorable to recent Permian deals

Deal makes ConocoPhillips a top Permian producer

ConocoPhillips expects to remain active in its Bakken and Eagle Ford Shale operations even after growing its Permian Basin profile through the acquisition of Shell’s entire portfolio in the West Texas/New Mexico play, ConocoPhillips’ top executive said Sept. 21.

Not registered?

Receive daily email alerts, subscriber notes & personalize your experience. Register Now

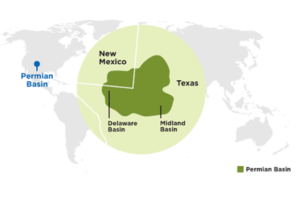

The giant play, the largest oil basin in the US with about 4.5 million b/d of oil output, will likely continue as a focus for the bulk of the company’s attention in the Lower-48 states even after the $9.5 billion Shell transaction, announced late Sept. 20, closes later in 2021, CEO Ryan Lance said in a webcast to explain the deal.

But the Bakken in North Dakota and the Eagle Ford in South Texas will remain “very competitive investments,” Lance said,

“We’re looking to ramp up a little bit of activity in both areas,” he said. “They are … very competitive on a cost-of-supply basis” — a crucial ConocoPhillips metric that is essentially the breakeven WTI oil price that yields a 10% return.

The company requires that metric at a price below $40/b for all Lower-48 operations to be competitive in its portfolio.

The Shell deal will add about 175,000 barrels of oil equivalent a day production and around 225,000 net acres in West Texas.

Before ConocoPhillips in January closed another big Permian acquisition of Concho Resources for about $9.7 billion — a deal that multiplied its Permian production nearly sevenfold — the Eagle Ford was the largest of the company’s “Big Three” Lower-48 operations.

But adding Concho’s more than 300,000 boe/d, ConocoPhillips’ Permian segment produced 435,000 boe/d in the second quarter. In addition, its Eagle Ford unit output was 227,000 boe/d and the Bakken was 95,000 boe/d.

Shell’s Permian portfolio will position ConocoPhillips alongside the very largest Permian operators with more than 600,000 boe/d, based on the Q2 output figures of both companies. ConocoPhillips expects Shell’s Permian operation to average about 200,000 boe/d of output alone in 2022.

Output mix is 50% crude oil

The production mix for the Shell assets is about 50% oil, with 25% each natural gas and NGLs, Lance said.

“The Permian is probably getting a bit more in the lion’s share of capital because of where the cost of supply sits,” said Lance. “But that’s not at the expense of the Eagle Ford and the Bakken. It’s probably at the expense of some other assets around the world.”

“We’re finding we’re getting more efficient and better at what we’re doing, so it takes less capital” to achieve the company’s strict metrics, he added.

In tandem with the Shell transaction, ConocoPhillips said it plans to raise its target level of asset dispositions to $4 billion-$5 billion by 2023 from a previously announced $2 billion-$3 billion. The additional $2 billion of planned asset dispositions will come mainly from the Permian Basin as part of the company’s ongoing high-grading of its portfolio.

“It’s going to be driven on what kind of assets we don’t think compete in the portfolio or to the right hand of our cost-of-supply curve,” Lance said.

He said the company has some of its own assets for sale “in the market right now,” including assorted acreage in the Permian, global assets, and Lower-48 assets.

“We should be taking things out of the right-hand side of the cost-of-supply curve and we should expect to continue to lower that, and [also] look for assets that don’t compete,” he said. “We expect we’re going to find some” in the Shell portfolio as well.

Despite its recent high-dollar Concho buy, analysts said ConocoPhillips’ victory in the sweepstakes to own Shell’s Permian assets, which that company had indicated earlier this year it would divest, was not unexpected.

Cash deal likely a plus

Not only has there been a “general cooling in the market” for shale acreage, and potentially fewer contenders, but ConocoPhillips’ ability to pay cash in a large deal likely was a major reason it was able to capture the assets for such a relatively modest price, said Andrew Dittmar, senior M&A analyst at Enverus.

ConocoPhillips’ reports price of about $15,000/acre for Shell’s position represents “a fraction of the nearly $60,000/acre Occidental paid for overlapping land in its purchase of Anadarko in 2019,” Dittmar said. Similarly, ConocoPhillips’ purchase of Concho also “priced attractively” at $10,000/acre,” he said.

Potential for new M&A record

S&P Global Platts Analytics data shows the Shell-ConocoPhillips deal puts US M&A activity this year at $47.2 billion, and on track to possibly set a new record in the shale era by year’s end, surpassing a record $53.5 billion seen in 2018.

In fact, Tim Leach, ConocoPhillips’ executive vice president of Lower 48 and former Concho CEO, said that had the ConocoPhillips-Concho deal not occurred when it did, neither company might have pursued the Shell assets separately.

The Shell assets were on Concho’s “wish list … for a long time,” before its merger with ConocoPhillips, Leach said, adding “it’s another strength of the combination” of the two companies that enabled the purchase.

While 50-50 operatorship of Shell’s Permian properties, primarily with Occidental Petroleum, has been “the knock-on this [prospective deal for would-be buyers] … it has generated free cash on shallowing underlying declines for the better part of two years,” Evercore ISI analyst Stephen Richardson said in a Sept. 21 investor note.

“ConocoPhillips is likely to transact/block up/clean up operatorship with plenty of trade bait to offer,” Richardson said.

Source: S&P Global

Energy News

Oil & Gas Permits

Author: phinds