OPERATIONAL HIGHLIGHTS

Average production for the quarter ended September 30, 2022 was 133,019 boe/d, comprised of over 80 percent oil and liquids.

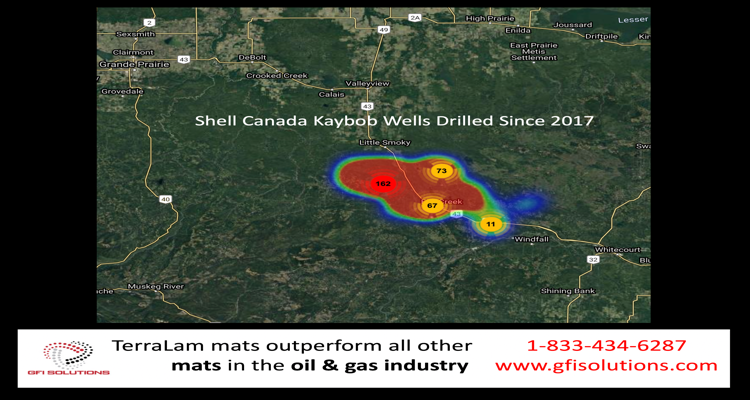

Crescent Point continues to generate strong operational results in its Kaybob Duvernay play, resulting in attractive asset level returns. The Company recently brought on stream its third fully operated multi-well pad achieving an average 30-day initial production (“IP30”) rate of approximately 900 boe/d per well (81% condensate, 5% NGL and 14% shale gas), which is expected to payout in approximately six months from the initial on-stream date at current commodity prices.

During third quarter, Crescent Point acquired additional lands in the Kaybob Duvernay for cash consideration of approximately $87 million. This acquisition included approximately 80 net sections of crown land with a 100 percent working interest, further expanding the Company’s drilling inventory in the play. Given its significant running room in the Kaybob Duvernay, Crescent Point expects to increase the proportion of capital it allocates to this high-return asset within its five-year plan. As a result, production in this area is expected to grow in a disciplined manner from approximately 35,000 boe/d in 2022 to over 50,000 boe/d by 2027, subject to commodity prices.

In its southeast and southwest Saskatchewan operations, Crescent Point continued to advance its decline mitigation projects during third quarter to further enhance long-term sustainability. This included secondary recovery waterflood programs and the initiation of a polymer flood, a tertiary form of recovery, within a unit in the Company’s Shaunavon play in southwest Saskatchewan.

Oil & Gas Permits Download

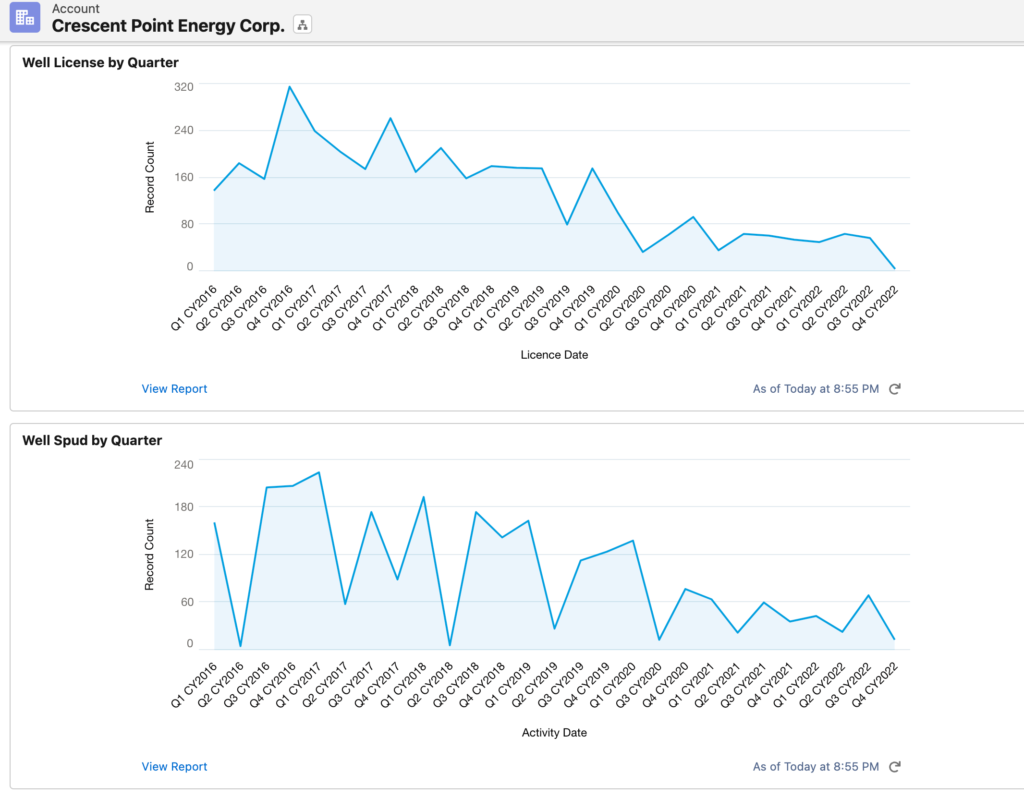

Crescent Point Wells Drilled 2022

During third quarter 2022, Crescent Point successfully drilled its first multi-lateral, open-hole horizontal well in its Viewfield Bakken play in southeast Saskatchewan with strong performance to-date. The Company is currently drilling a subsequent multi-lateral, open-hole horizontal well in the play. This innovation in well design removes the need for fracture stimulation and has the potential to expand the number of economic locations currently identified in the area.

Crescent Point’s continued commitment to strong environmental, social and governance (“ESG”) practices was recently recognized by Morgan Stanley Capital International (“MSCI”) Inc. which increased its rating to “AA”. This is the second consecutive year the Company has received an increase in its ESG Ratings assessment from MSCI Inc.

Crescent Point Well Permit Summary

2022 GUIDANCE

The Company’s 2022 development capital expenditures guidance has been slightly increased to $950 million, from $875 to $900 million previously. This increase reflects a higher inflationary cost environment and Crescent Point’s decision to maintain an active drilling rig in its Kaybob Duvernay and North Dakota plays where the Company is currently ahead of schedule on its 2022 drilling program. Crescent Point remains on track to meet its 2022 annual average production guidance, which is now at the mid-point of its prior range of 130,000 to 134,000 boe/d.

2023 GUIDANCE

Crescent Point plans to generate annual average production of 134,000 to 138,000 boe/d in 2023. Based on development capital expenditures of $1.0 to $1.1 billion, the Company expects to generate approximately $1.1 to $1.5 billion of excess cash flow at US$75/bbl to US$85/bbl WTI. The Company’s 2023 budget, including its base dividend, is fully funded at less than US$50/bbl WTI. Crescent Point expects to achieve this annual production guidance with spending toward the lower end of its budget based on projected costs in the current commodity price environment.

Crescent Point’s allocation of its 2023 budget is centered around risk-adjusted returns and remains focused within its four major operating areas. In the Kaybob Duvernay and North Dakota resource plays, the Company plans to operate a one rig drilling program with a focus on realizing additional efficiencies. Crescent Point’s Kaybob Duvernay budget is also expected to include a step-out drilling program to identify new potential drilling locations. In southeast and southwest Saskatchewan, the Company plans to continue to focus on low risk, high-return development, advancement of its decline mitigation programs and further expansion of the economic boundaries within these assets.

Consistent with its capital allocation framework, the Company plans to allocate approximately 15 percent of its 2023 budget to long-term projects to enhance its sustainability. Such projects include the continued advancement of various decline mitigation programs, such as waterflood and polymer floods, and environmental initiatives designed to reduce Crescent Point’s emissions and inactive well inventory.

OUTLOOK

Crescent Point continues to demonstrate strong operational and financial execution, while taking a disciplined approach to capital allocation and maintaining its commitment to returning a meaningful amount of capital back to shareholders.

The Company expects to generate significant excess cash flow of approximately $1.1 to $1.5 billion, based on its 2023 guidance at US$75/bbl to US$85/bbl WTI, allowing for significant returns to shareholders, including an expected further improvement in its leverage ratio to less than 0.3 times net debt to adjusted funds flow.

Approximately 15 percent of the Company’s total production is currently hedged in 2023, including over 20 percent in first half of the year. Crescent Point will remain disciplined in its hedging strategy in the context of market conditions.

In conjunction with its 2023 budget, the Company has updated its five-year outlook, which is expected to generate approximately $5.0 to $6.0 billion of cumulative after-tax excess cash flow from 2023 to 2027, at US$75/bbl to US$85/bbl WTI. Crescent Point’s five-year plan assumes annual average production increasing to approximately 145,000 boe/d by 2027, subject to commodity prices. This plan remains disciplined with a continued focus on returns and long-term sustainability.

Crescent Point remains in a strong financial position and is focused on creating long-term value for shareholders through a combination of returning capital and continually enhancing the sustainability of the business on a per-share basis.

Crescent Point Energy News

Crescent Point plans $1.05B to $1.15B in development capital expenditures in Canada for 2024

Crescent Point Announces Sale of its North Dakota Assets

Crescent Point Energy to buy Spartan Delta’s Montney assets for $1.2 bln

Crescent Point Announces Q3 2022 Results and 2023 Budget

Crescent Point Energy reports $1.18-billion first-quarter profit

Crescent Point Announces Q3 2021 Results

Crescent Point Energy Playbook

Crescent Point Energy Corp. First Quarter 2021 Update