Marathon Oil Corporation (NYSE: MRO) announced it has entered into a definitive purchase agreement to acquire the Eagle Ford assets of Ensign Natural Resources for total cash consideration of $3.0 billion. The transaction is subject to customary terms and conditions, including closing adjustments, and is expected to close by year-end 2022.

Highlights

“This acquisition in the core of the Eagle Ford satisfies every element of our exacting acquisition criteria, uniquely striking the right balance between immediate cash flow accretion and future development opportunity,” said chairman, president, and CEO Lee Tillman. “The transaction is immediately accretive to our key financial metrics; it will drive higher distributions to our shareholders consistent with our operating cash flow driven Return of Capital Framework; it’s accretive to our inventory life with high rate-of-return locations that immediately compete for capital; and it offers compelling industrial logic by nearly doubling our position in a Basin where we have a tremendous track record of execution excellence. Importantly, we expect to execute this transaction while maintaining our investment grade balance sheet and while still delivering on our aggressive return of capital objectives in 2022 and beyond.”

Oil & Gas Permit Download

Marathon and Ensign Wells Drilled 2020

Strategic Rationale

- Significant Financial Accretion: The transaction is immediately and significantly accretive to Marathon Oil’s key financial metrics, expected to drive a 17% increase to 2023 operating cash flow1 and a 15% increase to free cash flow1. The transaction was acquired at approximately 3.4x 2023 EBITDA1 and a 17% free cash flow yield1, accretive relative to Marathon Oil’s 2023 stand-alone metrics at the same price deck (4.7x EV/EBITDA2, 13% FCF Yield2).

- Enhances Return of Capital Profile: As the transaction is accretive to Marathon Oil’s cash flow profile, it will immediately enhance shareholder distributions, consistent with the Company’s transparent Return of Capital Framework that is uniquely driven by operating cash flow and, in a $60/bbl WTI or higher price environment, calls for at least 40% of annual operating cash flow to be returned to equity holders. More specifically, Marathon Oil expects the transaction to increase 2023 shareholder distribution capacity by approximately 17%1. Additionally, due to the cash flow accretive nature of the transaction, Marathon Oil expects to raise its quarterly base dividend an additional 11% post transaction close to 10ct/sh. Importantly, for full year 2022, Marathon Oil still expects to meet its objective to return at least 50% of adjusted operating cash flow to shareholders, outperforming its 40% framework minimum.

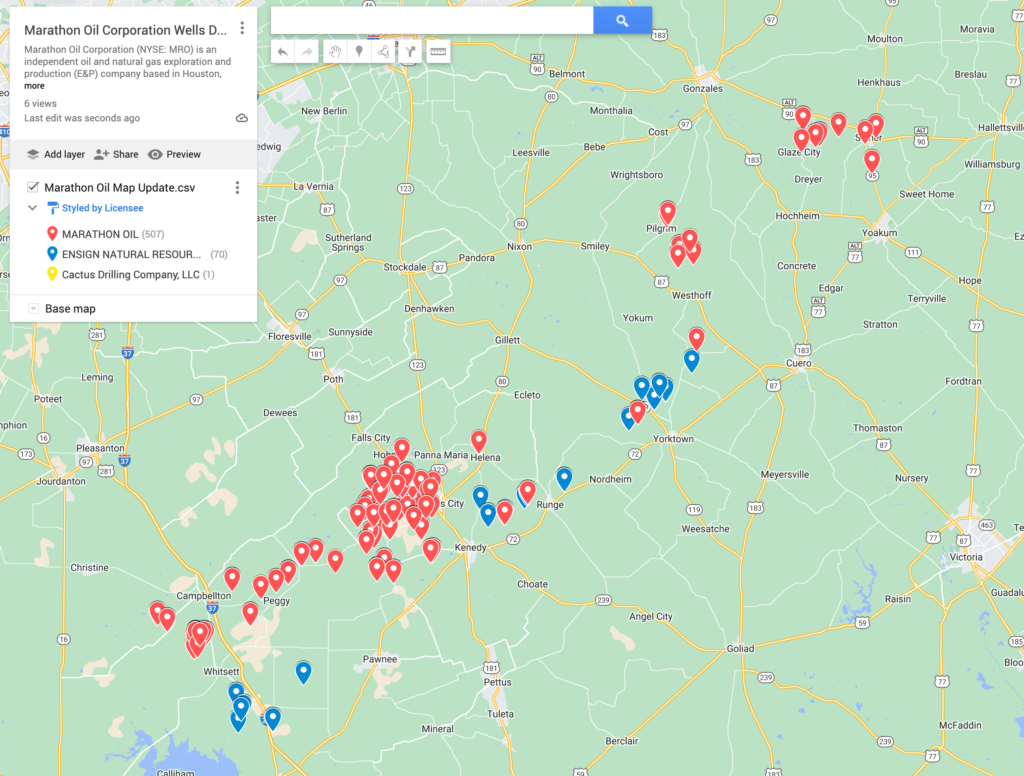

Map of Marathon Wells Drilled Since 2020 (click to access)

- Compelling Industrial Logic Expands Scale and is Accretive to Inventory Life and Quality: The transaction significantly expands Marathon Oil’s Eagle Ford position through the addition of 130,000 net acres with 97% working interest located primarily in the prolific condensate and wet gas phase windows of the play. The Company estimates it is acquiring more than 600 undrilled locations, representing an inventory life greater than 15 years, with inventory that immediately competes for capital in the Marathon Oil portfolio. The acreage is adjacent to Marathon Oil’s existing Eagle Ford position, enabling the Company to further leverage its knowledge, experience, and operating strengths in the Basin, while materially increasing its Basin scale to 290,000 net acres and contributing to optimized supply chain accessibility and cost control in a tight service market. The acquisition also includes 700 existing wells, most of which were completed before 2015 with early generation completion designs. These existing locations offer upside redevelopment potential, none of which was considered in the Company’s valuation of the asset or inventory count.

- Maintaining Investment Grade Balance Sheet: Marathon Oil expects to fund the transaction with a combination of cash on hand, borrowings on the company’s revolving credit facility, and new prepayable debt. The Company does not expect the transaction to meaningfully affect its leverage profile, continuing to expect a net debt to EBITDA ratio of less than one3, and coupled with enhanced enterprise scale anticipates positive credit quality implications.

Additional Transaction Details

The 130,000 net acres (99% operated, 97% working interest) Marathon Oil is acquiring from Ensign Natural Resources span Live Oak, Bee, Karnes, and Dewitt Counties across the condensate, wet gas, and dry gas phase windows of the Eagle Ford. Estimated fourth quarter 2022 oil equivalent production is 67,000 net boed (22,000 net bopd of oil). Marathon Oil believes it can hold fourth quarter production flat with approximately 1 rig and 35 to 40 wells to sales per year. The Company’s valuation of the asset was based off this maintenance level program and does not include any synergy credits or upside redevelopment opportunity. The transaction is expected to close by year-end 2022 with an effective date of Oct. 1, 2022. Acquired tangible assets are eligible for full expensing for the purpose of income tax optimization.

Energy News

Author: phinds