Company Links

Address

3800, 525 – 8th Avenue SW

Calgary, Alberta, Canada T2P 1G1

403-266-0767

Company Overview

Whitecap Resources is a Canadian public oil company based in Calgary, Alberta, with operations in Alberta, Saskatchewan, and British Columbia.

Resent News

Whitecap Resources’ 2025 budget allocates $1.1–$1.2 billion in capital expenditures, focusing on production growth, efficiency improvements, and infrastructure expansion. The company expects average production of 176,000 – 180,000 boe/d (63% liquids), driven by strong performance in the Montney, Duvernay, and Saskatchewan conventional plays.

Operations

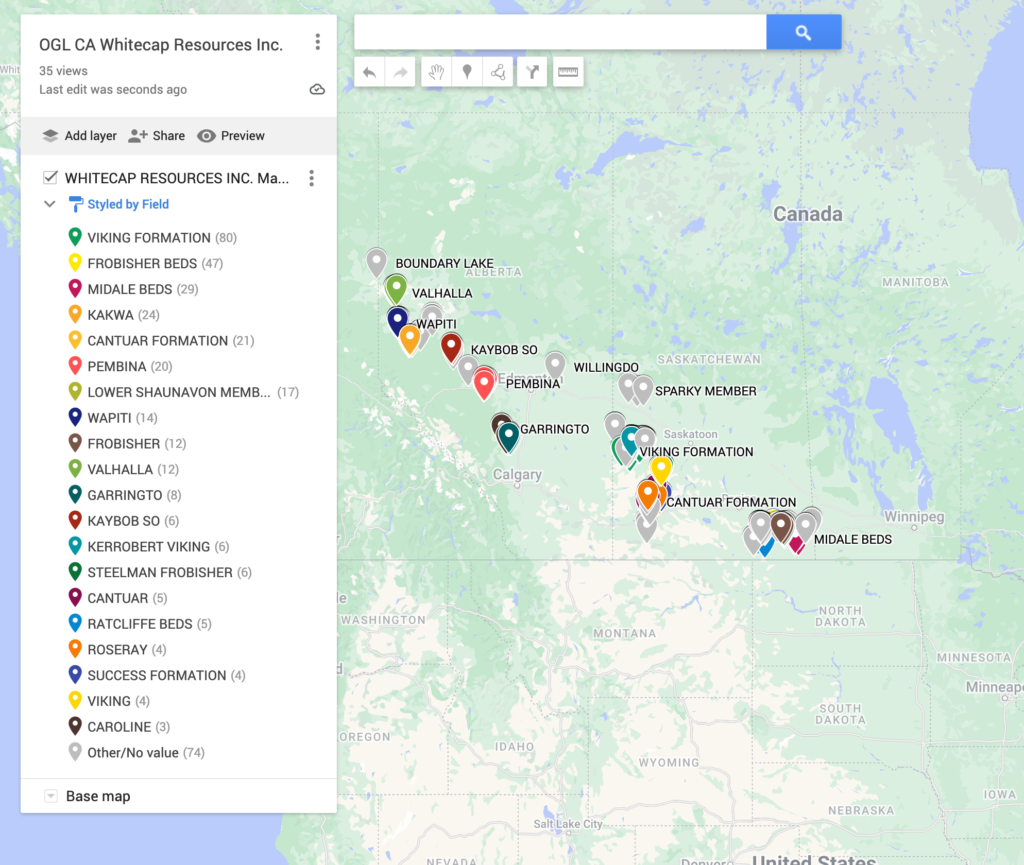

East Division – includes Central AB, West Sask, East Sask, and Weyburn regions, focusing on various oil plays and enhanced recovery methods. Central AB targets Cardium and Mannville assets with waterflooding and CO2 flood projects, while West Sask focuses on the Viking light oil play and Southwest Saskatchewan medium oil play with waterfloods and ASP floods. Weyburn is the world’s largest CCUS project, capturing over 40 million tonnes of CO2, and focuses on the Midale and Frobisher reservoirs.

West Division – consists of the Smoky, Kaybob, and PRA regions, focusing on condensate-rich natural gas and light oil plays. Smoky and Kaybob utilize pad-based horizontal drilling and multi-stage fracturing in the Montney and Duvernay resource plays, respectively. The PRA region, Whitecap’s original asset area, expands on Valhalla’s infrastructure through the Charlie Lake, Montney, and Cardium oil plays.

Permit Download Center

Whitecap Resources Wells Drilled 2024

Whitecap Resources Drilling Rigs Feb 2025

Whitecap Resources Facility Permits

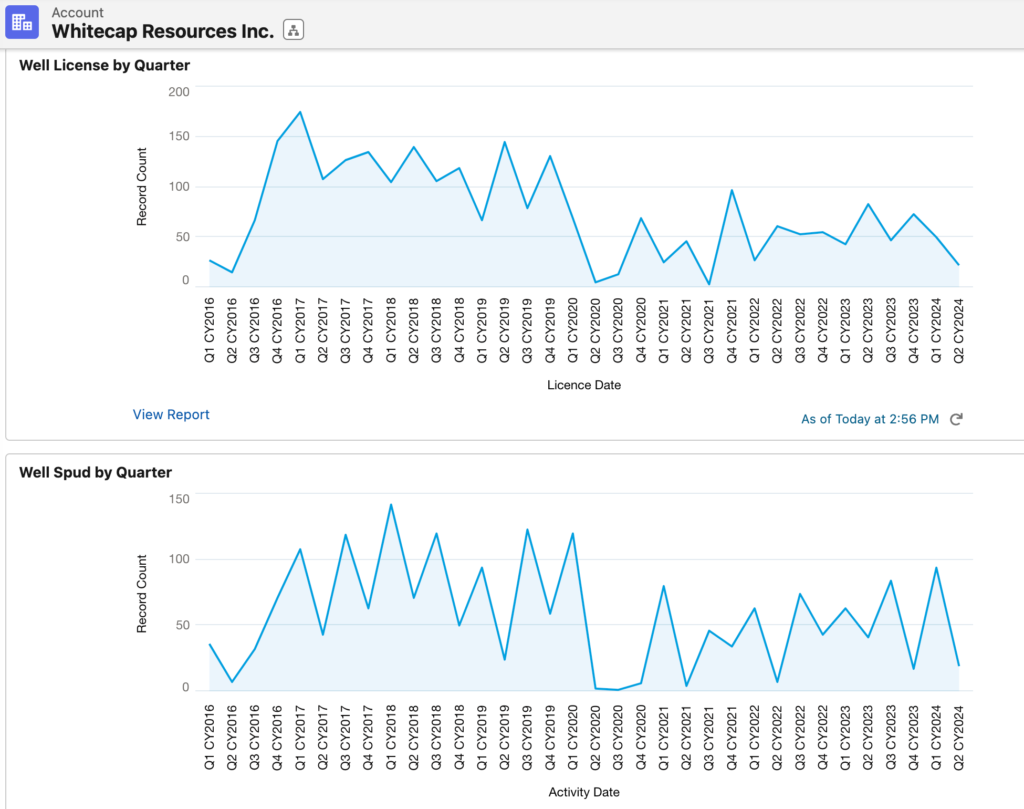

Well Permit Summary

Operations Map

Whitecap News

Author: phinds