As U.S. shale drilling matures and premium acreage depletes, the search for high-return, long-life resource plays is shifting northward. In a new white paper titled “What Remains: North American Upstream Inventory,” energy private equity firm Kimmeridge outlines which shale basins have the best runway for returns over the next 10 years—and why the spotlight is now turning to Canada.

Let’s break down what Kimmeridge says about each key basin and their evolving roles in the future of North American oil and gas.

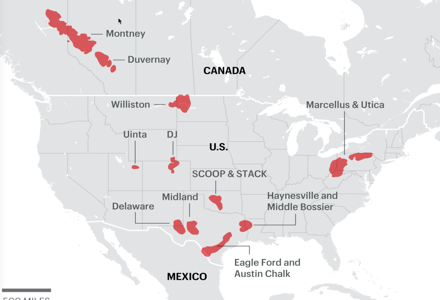

🇨🇦 1. Montney Shale (Alberta & British Columbia) — Future #1

Kimmeridge believes the Montney Shale is the most compelling basin in North America over the long term.

- Inventory Quality: Vast amounts of undeveloped, high-quality acreage remain.

- Development Pace: Much slower than the Permian, allowing the Montney to preserve its top-tier drilling opportunities.

- Gas-Weighted Play: Strong economics tied to growing LNG demand and export potential.

- Efficiency: Among the lowest breakeven costs in North America.

- Strategic Fit: Kimmeridge has already made a move via its investment in Advantage Energy.

“The Montney may sustain higher returns for longer,” says Kimmeridge, citing its balance of economic strength, longevity, and under-drilled profile.

As global gas demand rises and North American LNG expands, the Montney is ideally positioned to benefit—especially if Canadian pipeline politics loosen under new leadership.

🇺🇸 2. Uinta Basin (Utah) — The Emerging Sleeper

Rarely mentioned in past shale conversations, the Uinta Basin is quickly rising in strategic importance.

- Logistics Breakthrough: Recent rail expansions mean crude can now be transported more economically from this landlocked region.

- Light Oil & Condensate: Production is rich in high-value hydrocarbons.

- Undrilled Core: Much of the Uinta remains lightly developed.

- Regulatory Tailwinds: Utah offers a relatively stable regulatory environment for development.

Kimmeridge ranks Uinta #2 in its 10-year forecast, noting that improved takeaway capacity is unlocking a basin previously written off by operators.

This play may surprise the market as a future high-margin contributor, especially for nimble producers targeting niche barrels.

🇨🇦 3. Duvernay Shale (Alberta) — Undervalued and Underappreciated

The Duvernay is often overshadowed by its neighbor, the Montney, but Kimmeridge sees it as an undervalued gem.

- Resource Potential: Rich in liquids and natural gas, with strong EURs (estimated ultimate recoveries).

- Technology-Driven: Benefiting from U.S.-pioneered horizontal drilling and fracking.

- Less Competition: Limited large-scale development to date.

- Gas & Condensate-Heavy: Attractive to companies with LNG ambitions or condensate blending strategies.

While still early in its life cycle, the Duvernay offers optionality for producers and investors alike. Kimmeridge projects this basin to move into third place in well economics over the next decade.

🇺🇸 4. Delaware Basin (West Texas & New Mexico) — Slowing, But Still Strong

The Delaware Basin, part of the greater Permian, remains one of the top producers today—but with caveats.

- Today’s Economics: Top-tier wells with excellent returns—still the #1 or #2 play in 2024.

- Depth and Complexity: Delaware wells are deeper and more geologically complex than in the Midland.

- Gassier Rock: More natural gas than oil, affecting economics in a weak gas price environment.

- Infrastructure Gaps: Less developed takeaway and processing than the Midland.

- Regulatory Risk: Expands into New Mexico, where state rules can be less favorable.

“The Delaware will compete for longer,” says Kimmeridge, “but its high activity level is working against it.”

It remains a cornerstone of U.S. production, but its long-term advantage is fading as core locations are drilled at a rapid clip.

🇺🇸 5. Marcellus Shale (Pennsylvania) — The Gas Giant Plateau

The Marcellus Shale is North America’s largest gas play, and a global benchmark for shale efficiency.

- Best-in-Class Gas Economics: Among the lowest-cost dry gas basins in the world.

- Infrastructure Constrained: Permitting issues continue to bottleneck takeaway capacity.

- Political Friction: Local and state regulations frequently challenge new development.

- LNG Linkage: Still relatively limited exposure to export terminals compared to Gulf Coast gas basins.

Despite near-term constraints, the Marcellus remains a profit machine for incumbents. However, its future growth is capped unless new pipelines like Mountain Valley Pipeline (MVP) open up broader markets.

🧠 Final Thoughts: A Shift in Basin Leadership

Kimmeridge’s 10-year outlook reveals a strategic shift underway:

- 🛑 From the hyperactive U.S. Permian basins

- ✅ Toward slower-depleting, gas-weighted Canadian and emerging U.S. basins

With LNG export demand soaring and core U.S. acreage depleting, inventory life, basin depth, and export orientation are the new success metrics. This reordering of shale priorities could define the next phase of M&A, capital allocation, and midstream development.

🔍 Kimmeridge 10-Year Basin Ranking (2035 Outlook)

| Rank | Basin | Key Strengths |

|---|---|---|

| 1 | Montney | Efficiency, longevity, LNG alignment |

| 2 | Uinta | Logistics breakthrough, light oil |

| 3 | Duvernay | Rich resource base, early-stage upside |

| 4 | Delaware | High current activity, fading core |

| 5 | Marcellus | World-class gas, but constrained |

Kimmeridge is a New York-based alternative asset manager specializing in the energy sector, with a focus on unconventional oil and gas assets in North America. Founded in 2012 by Ben Dell, Dr. Neil McMahon, and Henry Makansi, the firm distinguishes itself through deep technical expertise, proprietary research, and a commitment to environmental responsibility.

Oil & Gas Account Directory

Author: phinds