Below we summarize recent (2024–2025) drilling activity, budget allocations, and production volumes in Oklahoma (primarily the Anadarko Basin and related plays) for six companies: Ovintiv, Mach Natural Resources, Devon Energy, Coterra Energy, Continental Resources, and Mewbourne Oil Company. Key metrics are compared in the table, followed by detailed highlights for each company.

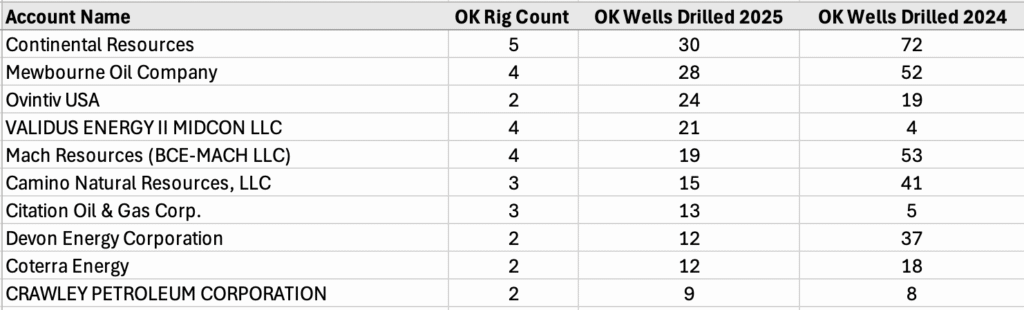

Top 10 Oparators in Oklahoma by Wells Drilled (June 2025)

| Company | Oklahoma Production | Oklahoma CapEx | Active Rigs (Drilling) |

|---|---|---|---|

| Ovintiv | ~91 MBOE/d (Q1 2025; ~55% liquids) | ~$300–$325 MM planned 2025 | ~1–2 rigs (added one in early 2025) |

| Mach Natural Resources (Mach) | ~86.7 MBOE/d (Q4 2024; 24% oil) | ~$260–$280 MM planned 2025 | ~1 rig (reduced from 2 in mid-2024) |

| Devon Energy | ~79 MBOE/d (Q1 2025; ~15% oil) | ~$150 MM planned 2025 | 2 rigs in 2025 (down from 3 in 2024) |

| Coterra Energy | ~64 MBOE/d (2024 avg) | ~$289 MM in 2024 | 1 rig at end-2024 (added rig in 2025) |

| Continental Resources (private) | ~32% of co. production from Anadarko (Q2 2024) | (N/A – private) | ~7–9 rigs in Oklahoma (2025) |

| Mewbourne Oil Co. (private) | (N/A – private; high gas focus) | (N/A – private) | ~7–9 rigs in Oklahoma (2025) (21 wells drilled in 2023) |

Note: MBOE/d = thousand barrels of oil equivalent per day. “Liquids” includes crude oil and NGLs. CapEx = capital expenditures. Anadarko Basin operations are primarily in Oklahoma (SCOOP/STACK plays), with some assets extending into southern Kansas and the Texas Panhandle in the case of Mach. Sources are cited in brackets.

Ovintiv (OVV) – Oklahoma (Anadarko Basin) Operations

Ovintiv (formerly Encana/Newfield) holds significant acreage in Oklahoma’s STACK/SCOOP (Anadarko Basin). The company’s Oklahoma activity has been more modest relative to its Permian and Montney operations, but Ovintiv is still investing in the play. In Q1 2025, Ovintiv’s Anadarko production averaged ~91,000 BOE per day (55% liquids). The company turned 10 net wells in line during Q1 and plans to bring 25–35 net wells online in 2025 in this area. Correspondingly, Ovintiv has budgeted roughly $300–$325 million of capital to Oklahoma (Anadarko) in 2025.

This plan represents a continued, albeit measured, program – likely equating to about 1–2 drilling rigs running. (Indeed, industry data indicates Ovintiv added an extra rig in Oklahoma early 2025 as gas prices improved.) Ovintiv’s focus in the play remains on core liquids-rich targets, but the Oklahoma assets are gas-weighted relative to its oilier plays. For context, Ovintiv’s total company production guidance for 2025 is ~600 MBOE/d, so the Anadarko contributes on the order of 15% of total output. Ovintiv’s CEO noted they remain committed to disciplined capital deployment across the portfolio, including the Anadarko, to deliver shareholder returns even as they maintain energy output.

Mach Natural Resources (Mach Resources) – Mid-Continent Focus

Mach Natural Resources (NYSE: MNR), led by CEO Tom L. Ward, is an upstream LP focused almost entirely on the Mid-Continent. Mach’s assets span the Anadarko Basin (Oklahoma & Kansas) and the Ardmore Basin (southern Oklahoma). Mach has rapidly become one of Oklahoma’s top producers after acquiring legacy assets and pursuing an income-focused strategy. In Q4 2024, Mach’s production averaged 86.7 MBOE/d (24% oil, 52% natural gas, 24% NGL), generating $241 million in revenue for the quarter. For full-year 2024, Mach’s output averaged roughly in the low-80s MBOE/d, reflecting its significant scale in Oklahoma.

Drilling activity: Mach drilled 11 gross (9 net) wells and brought 10 gross (8 net) wells online in Q4 2024. However, faced with weak gas prices in mid-2024, Mach intentionally cut its operated rig count from 2 rigs down to 1 rig (specifically in the Oswego formation) to reduce expenditures. This decision prompted a ~15% cut to Mach’s 2024 capital budget, illustrating their “disciplined reinvestment rate” philosophy. By year-end 2024, Mach had 5 net wells in progress and one active rig.

Budget and 2025 outlook: Mach’s capital spending in 2024 totaled about $60 million in Q4 (including $56 MM on upstream development). For full-year 2025, Mach guides to $260–$280 million in total development capital and forecasts production to average 79–83 MBOE/d. This suggests a relatively flat-to-slightly lower production profile year-over-year, consistent with running roughly one rig. Tom Ward emphasized that Mach’s strategy is to maximize cash distributions to investors while maintaining low leverage, rather than chase high growth. Even so, Mach continues to “dig in” on its Midcon assets at a time when many peers had fled – a point noted by industry observers.

Devon Energy (DVN) – Anadarko (STACK) Asset Highlights

Devon Energy, an Oklahoma City-based independent, maintains a significant position in the Anadarko Basin (STACK play) alongside its larger operations in the Delaware Basin, Williston Basin, etc. The Oklahoma assets have become more gas/NGL-oriented over time, but remain a key component of Devon’s portfolio. In Q1 2025, Devon’s company-wide production averaged 815,000 BOE/d across all regions (Delaware, Williston/Rockies, Eagle Ford, and Anadarko). The Anadarko Basin contributed roughly ~79,000 BOE/d of that (approximately 10% of Devon’s total output). Notably, the Anadarko production mix is heavily natural gas and NGLs, with only on the order of 14–16% oil – reflecting the liquids-rich gas character of the STACK’s Woodford/Meramec formations.

Drilling and capex: Devon significantly scaled down activity in Oklahoma last year in response to low gas prices. In 2024 they averaged 3 operated rigs in the Anadarko, but for 2025 the plan is to run ~2 rigs on average. The company brought 66 gross operated wells online in 2024 in the play, but plans to drop to only ~30 wells in 2025 – a sharp activity reduction. Accordingly, Devon’s capital investment in the Anadarko is projected at ~$150 million in 2025, down from roughly $200 million in 2024. (For context, Devon’s total 2025 capex guidance is $3.6–$3.8 billion, so the Oklahoma share is relatively small.)

Despite the pullback, Devon signaled renewed interest in its Oklahoma acreage going forward. In fact, Devon extended its drilling joint-venture with Dow in the STACK, adding 49 new well locations under the JV (with ~$40 million carry from Dow) and plans to resume development in Blaine County in Q2 2025. This indicates Devon is ready to “dial up” activity in Oklahoma when economics justify it. Devon’s leadership noted that, while the Delaware Basin is the growth engine, the Anadarko Basin remains a strategic part of the portfolio that they can ramp up or down as needed. Indeed, after a strong Q1, Devon modestly raised its 2025 production outlook and cut capital $100 MM due to efficiency gains, highlighting the flexibility and cost focus that could benefit its Oklahoma operations as gas prices recover.

Coterra Energy (CTRA) – Oklahoma (Anadarko) Segment

Coterra Energy was formed from the 2021 merger of Cimarex and Cabot. While Coterra is chiefly known for its Permian (Delaware Basin) and Marcellus gas assets, it also inherited legacy Oklahoma assets (Anadarko Basin) from Cimarex. These are primarily in the Cana-Woodford (STACK) and Arkoma/Woodford areas of Oklahoma. Coterra’s 2024 net production in the Anadarko Basin averaged ~64 MBOE/d, which was about 9% of the company’s total equivalent production. (On a 6:1 basis that was 64 MBOE/d; on a 20:1 economic basis, 41 MBOE/d or ~12% of total, underscoring the gas-heavy nature of these volumes.) Coterra’s Oklahoma output is indeed gas/NGL-rich, with development focused on the Woodford Shale and Meramec formations.

Capital and activity: In 2024, Coterra invested $289 million in drilling and completions in the Anadarko Basin. By year-end 2024, Coterra had just 1 drilling rig running in Oklahoma and no active frac crew (essentially pausing growth amid low prices). Approximately 527 net wells produce for Coterra in the Anadarko, of which 62% are operated by the company. Going into 2025, Coterra indicated it would flex its activity in Oklahoma according to gas market conditions. With natural gas prices rebounding to ~$4, Coterra and a few other public operators brought back at least one rig to the Anadarko in early 2025. This suggests Coterra is ramping from 1 to perhaps 2 rigs in Oklahoma to carefully resume development. The company has not provided explicit 2025 Anadarko capex guidance publicly, but given 2024’s spend and the early-2025 uptick, a ballpark figure in the low-to-mid $200 millions is likely if that extra rig is sustained. Coterra’s portfolio flexibility was highlighted by management – they curtailed Marcellus drilling in 2024 and can similarly adjust Oklahoma activity up or down. The firm remains “built for the future” with a diversified base, and Oklahoma’s STACK is one lever they can pull when economics improve.

Continental Resources (CLR) – SCOOP/STACK Leader in Oklahoma

Continental Resources, founded by Harold Hamm, is the largest operator in Oklahoma’s modern oil & gas plays. Continental has long dominated the SCOOP/STACK activity and, unlike many peers, “never stopped drilling the Anadarko” even during downturns. As a result, Continental led the state in wells drilled in 2024, significantly outpacing other operators like Mewbourne and Mach. Industry data shows Continental and Mewbourne each running on the order of 7–9 rigs in Oklahoma throughout early 2025 – far more than any other operators. This consistent drilling program reflects Continental’s commitment to the Mid-Continent core.

In terms of production, Continental’s Oklahoma assets (SCOOP & STACK) are prolific. Roughly one-third (32%) of Continental’s total production comes from the Anadarko Basin (Oklahoma). Given Continental’s total company output (which includes its large Bakken position) is estimated around ~400–450 MBOE/d in recent quarters, the Oklahoma share likely exceeds 130,000 BOE/d. Continental’s Oklahoma production is a mix of crude oil and rich gas; the SCOOP, for example, yields significant natural gas and condensate, while the STACK areas yield more oil and NGLs. The company does not break out public financials since going private in late 2022, but prior reports and investor calls indicated substantial capital allocation to Oklahoma. For instance, in 2021–22 when public, Continental was spending nearly half its drilling budget in Oklahoma. Even post-privatization, Continental reportedly continues hefty investment in its home state fields – their 2023 drilling count (dozens of wells) and sustained rig fleet confirm this. The scale of Continental’s program (363 wells drilled in 2023 across the company) and its recent 26% year-over-year production growth in Q4 (partly due to Oklahoma) underline that Oklahoma remains a growth engine for them.

Continental’s management has expressed long-term confidence in Oklahoma’s geology. They emphasize focusing on the core of the play (rather than fringe areas) and applying improved completions and spacing to maximize returns. In mid-2024, Continental told investors that 32% of its production was from Anadarko Basin and that it was still finding opportunity there despite the challenges others faced. In summary, Continental remains the anchor operator in Oklahoma, with the highest drilling activity and one of the highest production volumes in the state’s shale plays.

Mewbourne Oil Company – Aggressive Private Driller in Western OK

Mewbourne Oil Co. is a large private E&P traditionally known for its Permian Basin operations, but it has also emerged as a major driller in Oklahoma’s Anadarko region. In fact, Mewbourne is now one of the most active private drillers in Oklahoma, second only to Continental in recent rig count. Through 2024 and into 2025, Mewbourne has been running approximately 7–9 rigs in Oklahoma (focused on western Anadarko counties). This represents a significant ramp-up in Mid-Continent activity for the company. For example, in the Cleveland formation (Western Anadarko), Mewbourne doubled its new well count from 11 wells in 2022 to 21 wells in 2023. This surge in drilling reflects growing confidence in the play’s economics.

Not only has Mewbourne drilled more wells, but well performance has improved markedly – their average 90-day cumulative production per well jumped by 44% in 2023 vs. prior results. Higher oil prices and improved techniques have spurred a “renaissance” in the western Anadarko, and Mewbourne is at the forefront of this resurgence. The company’s focus in Oklahoma includes targets like the Cleveland and Tonkawa sands in counties such as Roger Mills, Ellis, Custer, Dewey, Beckham, and Caddo. These are shallower, liquids-rich formations on the Anadarko Basin’s northwest shelf, which Mewbourne can drill relatively economically.

As a private company, Mewbourne’s exact production volumes are not publicly disclosed, but given its drilling pace and well results, the company’s Oklahoma output is substantial and growing. Mewbourne’s success is such that it has been highlighted as helping spearhead a “new era of growth” in the region alongside Devon and others. By early 2025, industry analysts noted Mewbourne’s steady 7–9 rig program was maintaining a “strong presence” in Oklahoma. This solidifies Mewbourne’s role as a key player in Oklahoma’s oil and gas industry, even without public financial reports. Their strategy appears to be aggressively developing high-quality acreage (often acreage picked up during downturns) and leveraging their operational expertise honed in other basins.

In summary, Mewbourne and Continental have effectively filled the void left by some public operators that retreated from Oklahoma. Both are privately held and have kept Oklahoma drilling activity robust through 2024–25. Meanwhile, Ovintiv, Devon, and Coterra represent the public E&Ps that still invest in Oklahoma, though generally at a smaller scale and with a gas-focused approach, adjusting capital based on market conditions. Mach Resources stands out as a yield-focused operator concentrated entirely in Oklahoma, sustaining sizable production while carefully modulating its rig count. All together, these companies’ 2025 plans show a cautiously optimistic outlook for Oklahoma’s oil & gas sector – with drilling activity ticking up in response to better gas prices, but capital discipline remaining a common theme. The core Oklahoma plays (SCOOP/STACK and adjacent areas) continue to produce significant oil and (especially) gas volumes, contributing meaningfully to each company’s portfolio and to the state’s output.