The outlook for Western Canada’s heavy oil sector in 2025 is decisively optimistic. After years of volatility and infrastructure constraints, a new wave of investment and activity is materializing—driven by strong operator sentiment, a rebound in permitting, and a long-awaited breakthrough in market access: the Trans Mountain Expansion (TMX) pipeline.

Heavy Oil Market Intel Kit – Only $25

Includes – Heavy Oil Account List, Rig Report, Wells Drilled 2025 and Well Permits 2025

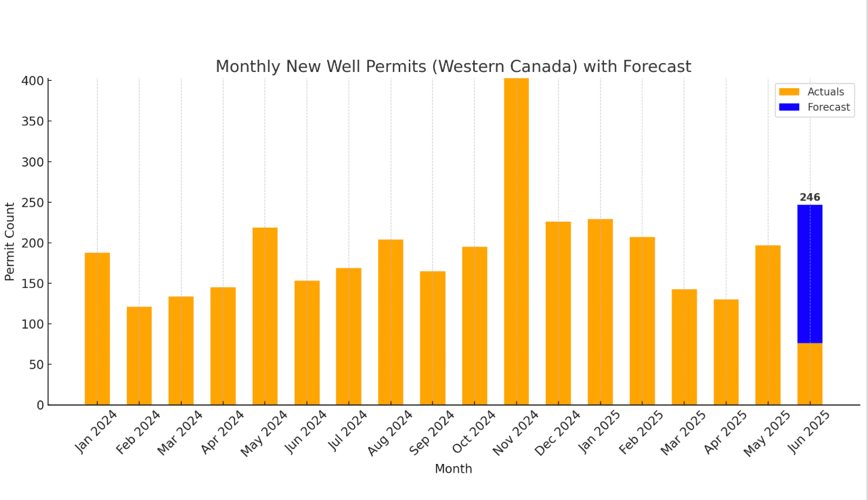

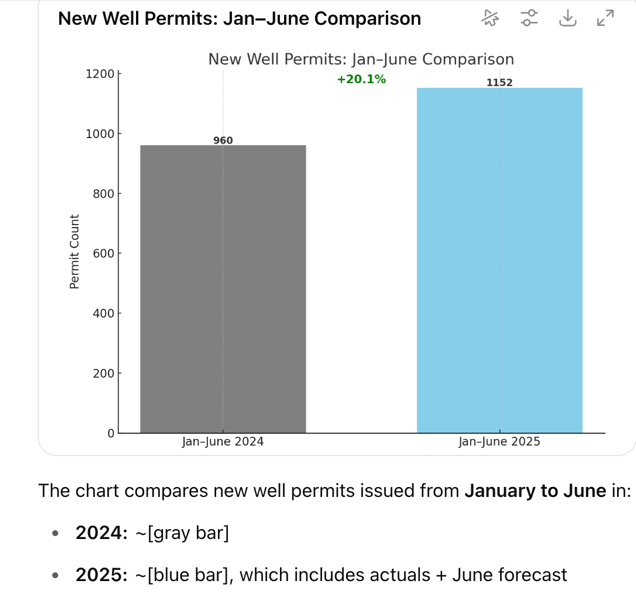

📈 Permit Activity Signals Recovery

New well permit data across the heavy oil region of Western Canada shows a significant increase in activity for the first half of 2025.

- Permits from January to June 2025 are up ~20% compared to the same period in 2024 (based on actuals plus forecasted June volumes).

- The trend is consistent across key producing areas such as Lloydminster, Cold Lake, and Peace River.

This upswing in permits aligns with broader capital plans from oil sands and thermal oil producers signaling renewed confidence in long-cycle heavy oil assets.

🛢️ Operator Strategies Reflect Growth and Efficiency

Here’s a snapshot of what leading heavy oil players are planning in 2025:

Company 2025 Production (bbl/d) 2025 CapEx (C$B) Strategic Focus Cenovus Energy 615–635K ~2.7–2.8 Optimization + brownfield growth CNRL 810–835K ~2.8 Maximize volumes, minimal downtime Suncor Energy 765–785K ~6.2 Cost control, reliability Imperial Oil 400–430K ~2.0 Existing asset optimization Strathcona 140–150K 1.35 Thermal oil growth + M&A Rubellite ~8.3K 0.07–0.09 Clearwater drilling + pilot innovation MEG Energy ~100K 0.635 Steady ops + phased expansion

These strategies indicate a measured return to growth, with a strong emphasis on thermal recovery, incremental expansion, and infrastructure leverage.

🚛 TMX Pipeline: The Game-Changer

The most significant tailwind for 2025 is the full in-service status of the Trans Mountain Expansion (TMX). With 590,000 bbl/d of new capacity flowing to tidewater, the pipeline:

- Alleviates the takeaway bottleneck that plagued Western Canadian Select (WCS) differentials

- Unlocks higher netbacks for oil sands producers

- Strengthens Canada’s export position to Asia-Pacific markets via Burnaby, BC

The TMX effect is already being priced into capital plans. Companies like Cenovus, MEG, and Strathcona are positioning to capitalize on improved margins and global access.

🧠 Outlook: Efficiency + Expansion = Resilient Growth

In contrast to the boom-bust cycles of the past, the 2025 outlook reflects disciplined expansion, capital efficiency, and a measured response to enhanced egress.

Key themes include:

- Growth via existing facilities (e.g., Narrows Lake, Christina Lake)

- Strategic well pad expansions rather than greenfield megaprojects

- Innovation in drilling (e.g., oil-based mud, waterflood pilots)

- Consolidation momentum (e.g., Strathcona’s bid for MEG)

As heavy oil reasserts itself in the global mix—particularly amid Venezuelan and Mexican decline—Western Canada is well-positioned to benefit.

🛢️ Final Word

With strong permit growth, confident operator strategies, and the TMX finally online, 2025 is shaping up to be a transformative year for heavy oil. For producers, service providers, and investors, the message is clear:

Western Canadian heavy oil is back—and this time, it’s built on access, efficiency, and strategy.